Increasing access to climate finance for small and medium businesses

Increasing access to climate finance for small and medium businesses

The capacity for micro, small and medium enterprises to realise their potential role in climate action is restricted by a lack of access to climate finance. Ellie Marsh and James Eustace of Dalberg discuss approaches to increase lending to these businesses, drawing from a recent CDKN-funded report.

An adequate response to the growing threat of climate change in developing countries requires greater involvement of the private sector – particularly micro, small and medium-sized enterprises (MSMEs). MSMEs account for 90% of businesses in developing countries and so greening MSMEs will be essential to help move the private sector to a low-emission, climate resilient development pathway. MSMEs also play an essential role in several climate technology sectors and help provide related goods and services to the poorest socioeconomic groups, which could help to improve the resilience of those most vulnerable to climate change.

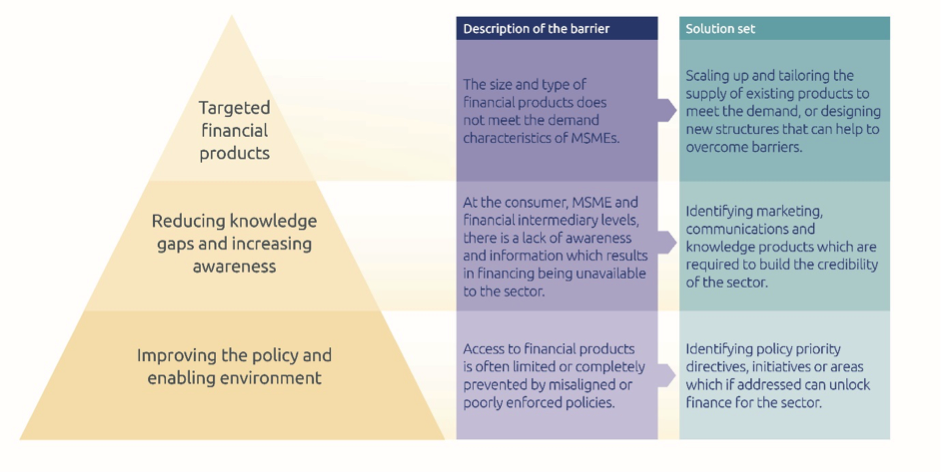

However, the capacity for MSMEs to realise their potential role in climate action is restricted by a lack of access to climate finance. This is primarily due to weak enabling environments, limited knowledge and awareness of finance opportunities, and inappropriate financial products (Figure 1). CDKN’s recently published report, “Increasing Access to Finance for MSMEs", assesses these barriers in detail and proposes a range of supporting interventions to address each of these barriers.

One of the key barriers to adequately increasing MSME involvement in climate action is successfully involving the informal sector. The majority of MSMEs in developing countries - almost 300 million - are in the informal sector, and cannot access credit using traditional approaches. Typically, informal businesses do not have sufficient collateral or credit history to secure debt and do not have sufficient capacity to meet application or reporting criteria for financial intermediaries. Therefore, access to climate finance will remain limited unless providers find a way of investing in informal businesses that goes beyond traditional financial products.

There are a variety of non-traditional lending approaches that use information other than financial statements or traditional collateral to assess repayment prospects of MSMEs. Some of these approaches include:

- Small business credit scoring, which uses information about the business owner, such as past spending history, and the firm to predict MSME loan performance;

- relationship lending which uses soft information on the MSME, such as strength of the management team or performance of the business as assessed by suppliers and customers, to predict MSME loan performance;

- factoring which uses valuations of the accounts receivable to evaluate repayment prospects;

- asset based lending which uses valuations of the assets pledged to evaluate repayment prospects; and

- leasing which uses valuations of the assets leased to evaluate repayment prospects.

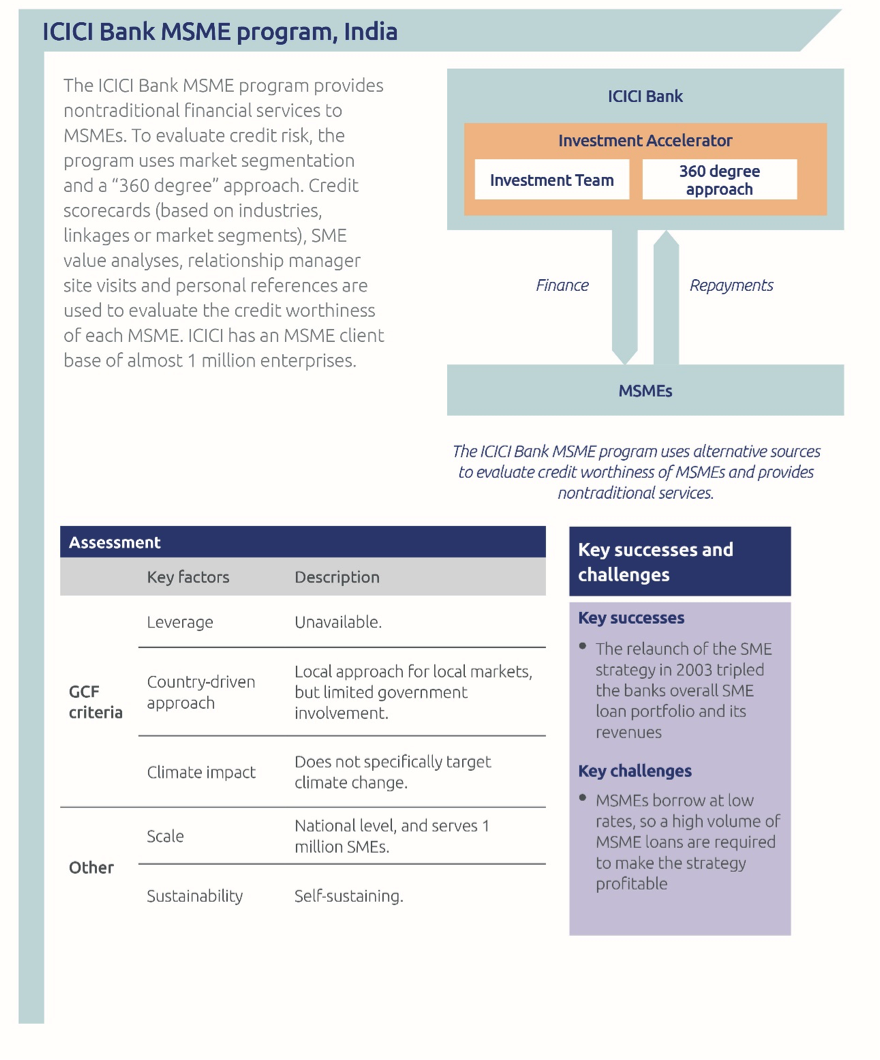

Financial institutions have successfully used a range of these approaches to lend to MSMEs. The ICICI Bank in India, for example (Figure 2), uses non-traditional lending approaches to provide financial services to MSMEs. To evaluate credit risk, the programme assesses multiple aspects of the MSME to evaluate its credit worthiness, which includes relationship manager site visits, personal references and valuation of the company. Since relaunching its SME strategy to incorporate this less traditional assessment programme, the overall size of the SME loan portfolio (along with its revenues) has tripled. Used more widely, this approach could help financial institutions to profitably provide loans to MSMEs for climate activities.

Figure 2: Overview of the ICICI Bank MSME Program, India

The use of alternative lending approaches is just one of many possible interventions that could help to increase MSME involvement in climate action. Interventions outlined in the report address barriers across the MSME finance chain and aim to increase the flow of finance from investors, through intermediaries and to MSMEs.

Read the MSME Policy Brief